1. Global Prices: NY11 Slips Under Macro Pressure

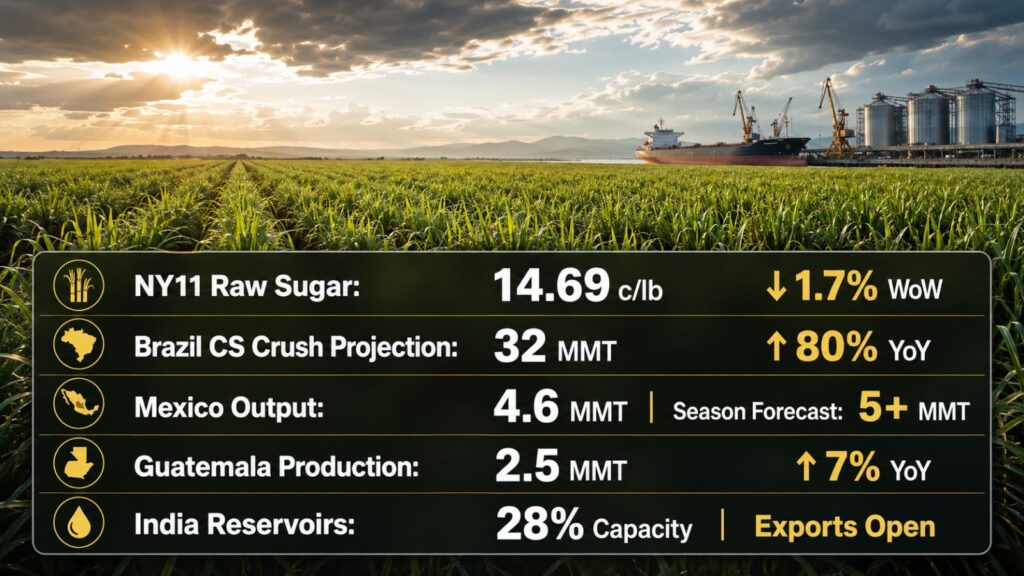

Raw sugar futures closed the week at 14.69 c/lb on the NY11 benchmark, down 1.7% week-on-week. The decline was driven by weakening oil and ethanol markets, which weigh heavily on the sugar price outlook given Brazil’s dual-use cane model.

While lower prices theoretically encourage a higher sugar mix in Brazil, millers are not reacting mechanically. They continue to factor in the full economic value of ethanol production – including vinasse output, lower processing costs, and on-site electricity generation – before adjusting their allocation.

The anticipated approval of Brazil’s E32 gasoline blend mandate – which would raise the compulsory ethanol content in fuel – was postponed during the week. This leaves a key demand-side variable unresolved and keeps market sentiment cautious heading into the second half of the season.

2. Brazil (Center-South): A Strong Opening to the Crush Season

Brazil’s Center-South – the world’s largest sugar-producing region – has opened the 2026 season with considerable momentum. Early-season cane crush is projected above 32 MMT, an 80% increase year-on-year, reflecting both a faster harvest start and improved cane availability compared to last season.

The sugar mix is estimated at approximately 37%, slightly below last year’s level. This reflects the ongoing uncertainty around ethanol returns rather than a firm directional shift. Hydrous ethanol is currently trading at R$2.27 per litre, down 17% year-on-year – further compressing the ethanol premium and potentially supporting a higher sugar allocation as the season progresses.

For B2B buyers sourcing raw sugar from Brazil, the key watch point is the resolution of the E32 mandate. If ethanol demand support remains absent, the sugar mix in H2 2026 could rise meaningfully – with implications for available export volumes.

3. India: Exports Remain Open, But Producer Sentiment Flags a Medium-Term Risk

India’s crop conditions remain stable. Reservoir levels are currently at 28% capacity – a healthy position for this time of year – providing adequate water availability to support the standing cane crop going into the next production cycle.

The government has confirmed no immediate plans to restrict sugar exports, despite a year of reduced domestic output. This is a positive signal for buyers in the Gulf and East Africa who rely on Indian supply as part of their procurement mix.

However, the medium-term picture warrants attention. Cane producers have formally expressed dissatisfaction with the government’s Fair and Remunerative Price (FRP) increase for the 2026/27 season, viewing it as insufficient given current input cost pressures. If this sentiment persists, it could discourage cane planting in the next cycle – a supply risk that is worth factoring into longer-horizon procurement planning.

4. The Americas: Mexico Outperforms; Guatemala Leads on White Sugar

Mexico continues to deliver above expectations this season. Cumulative sugar output stands at 4.6 MMT, with the full season now expected to exceed 5 MMT. Strong cane availability is likely to extend the harvest into June, adding further volume to an already solid season. On the policy side, the Mexican government announced a new initiative to promote the use of natural Mexican sugar over industrial sweeteners – a move that could gradually reduce export availability as domestic use is prioritised.

Guatemala recorded 2.5 MMT in sugar production for the season, up 7% year-on-year, with white sugar driving the majority of the growth. This is a constructive signal for buyers seeking refined product from Central America. Nicaragua, by contrast, is expected to fall short of earlier estimates, with output now projected at around 736 KT.

On balance, the Americas supply picture is favourable for procurement in Q2 and Q3 2026. Mexico’s extended harvest and Guatemala’s refined sugar output provide useful sourcing optionality for GCC and East African buyers.

5. EU & UK: Aphid Infestations Pose an Early but Real Risk to Beet Yields

Attention in Europe has shifted to crop protection, with rising aphid infestations emerging as a credible threat to beet yields this season. France and Belgium – two of the EU’s most significant beet sugar producers – have both reported elevated aphid pressure during a critical stage of crop development.

The situation is made more difficult by regulatory limits on insecticide use. A number of affected farmers have already reached the ceiling of their permitted applications under EU crop protection rules, leaving them with limited options should infestations intensify through the summer.

If pest pressure persists into the key summer growth period, the resulting reduction in beet tonnage could tighten EU white sugar supply in H2 2026. Buyers with exposure to European supply chains should track this closely through June, as any material yield shortfall would likely support white sugar premiums and affect import demand across the broader market.